If you have ever applied for a loan, credit card, or EMI service in India, you may have heard the term “CBIL score.” Many people search for CBIL online when they actually mean CIBIL. However, because “cbil” has become a commonly searched keyword, understanding what it means is important for beginners who want to improve their financial knowledge.

In simple words, CBIL usually refers to the CIBIL score, which is a three-digit credit score used by banks and financial institutions to evaluate your creditworthiness. Your credit score plays a major role in deciding whether you will get a loan, the interest rate you will pay, and the overall trust banks place in you.

In this detailed guide, we will explain everything about cbil, including:

- What is cbil?

- What is a CBIL score?

- How does it work?

- Why is it important?

- How to check your CBIL score?

- How to improve your score?

- Common mistakes that damage your credit profile

- Difference between CBIL and CIBIL

- Frequently asked questions

By the end of this article, you will fully understand how the cbil system works and why maintaining a good credit score is essential in today’s financial world.

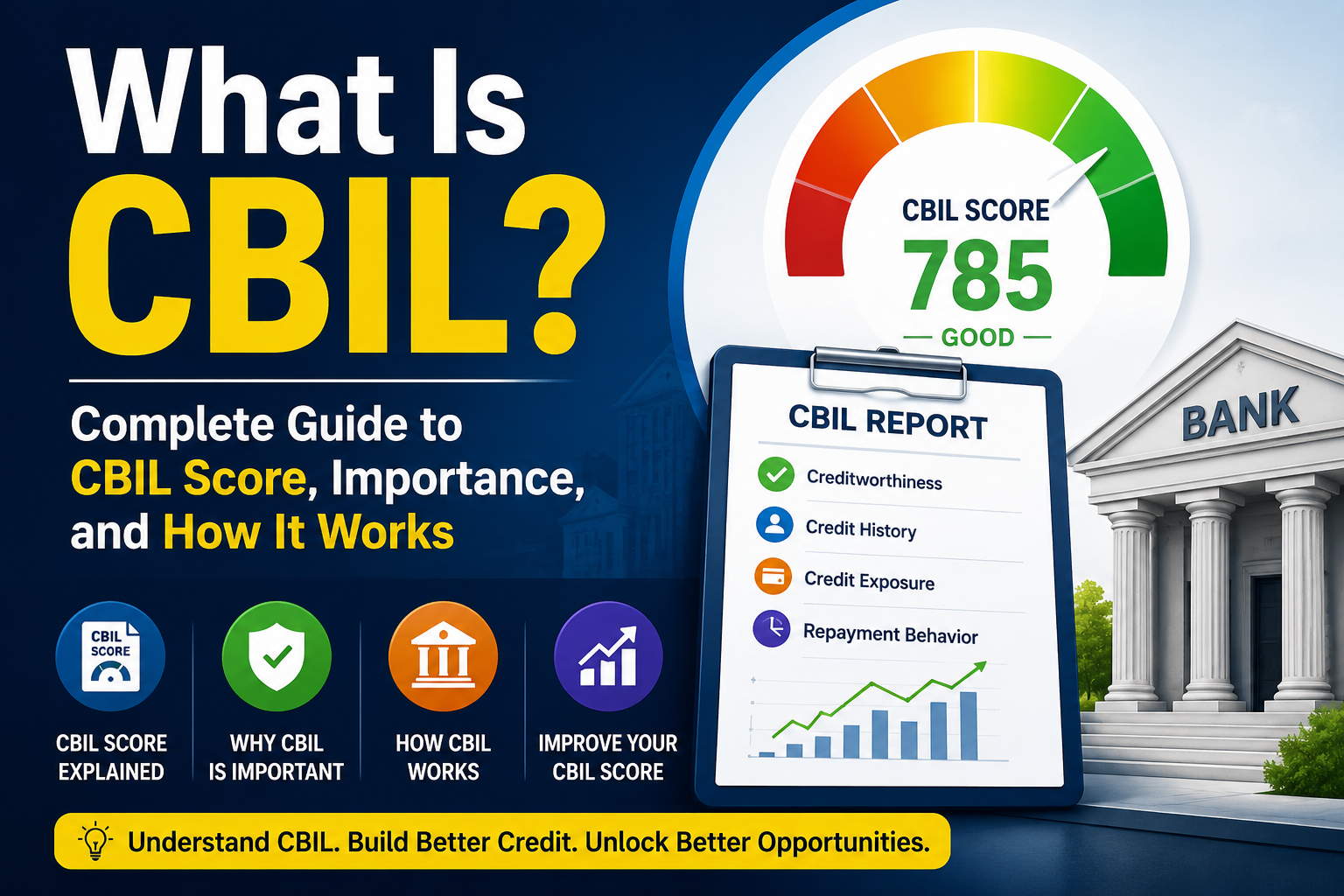

What Is CBIL?

CBIL is a commonly searched spelling variation of CIBIL. The correct term is CIBIL, which stands for Credit Information Bureau (India) Limited.

CIBIL is India’s first credit information company that collects and maintains records of individuals’ and companies’ credit-related activities. It tracks your loans, repayment history, credit cards, EMIs, defaults, and financial behavior.

Whenever you take a loan or use a credit card, banks send your financial data to CIBIL. Based on this information, a credit score is generated.

This score helps lenders determine whether you are financially responsible or risky.

For example:

- If you pay EMIs on time, your score improves.

- If you miss payments, your score decreases.

- If you use too much credit, your score can also go down.

Today, almost every major bank and NBFC in India checks your CBIL or CIBIL score before approving loans.

What Is a CBIL Score?

A CBIL score is a three-digit number ranging between 300 and 900.

This score represents your creditworthiness.

The closer your score is to 900, the better your financial profile appears to banks.

CBIL Score Range Explained

| Score Range | Meaning |

|---|---|

| 750 – 900 | Excellent |

| 700 – 749 | Good |

| 650 – 699 | Average |

| 550 – 649 | Poor |

| Below 550 | Very Risky |

A score above 750 is generally considered very good in India.

With a high score, you may get:

- Faster loan approval

- Lower interest rates

- Higher credit card limits

- Better loan offers

- Easier approval for home loans and car loans

On the other hand, a low score may lead to:

- Loan rejection

- Higher interest rates

- Lower credit limits

- Difficulty getting credit cards

That is why maintaining a healthy cbil score is extremely important.

How Does CBIL Work?

To understand cbil properly, you need to understand how the credit system functions.

Here is the step-by-step process:

1. You Borrow Money

You take:

- A personal loan

- Home loan

- Car loan

- Credit card

- Buy Now Pay Later service

- EMI purchase

2. Bank Reports Your Activity

The bank or lender sends your repayment information to CIBIL regularly.

This includes:

- Total loan amount

- EMI payments

- Missed payments

- Outstanding balance

- Credit card usage

- Loan closure status

3. CIBIL Generates Your Credit Profile

Using your financial history, CIBIL creates your credit report and assigns a credit score.

4. Lenders Check Your Score

Whenever you apply for a new loan, the lender checks your cbil score before approval.

If your score is high, the lender trusts you more.

If your score is low, the lender may see you as financially risky.

Why Is CBIL Important?

In today’s digital financial system, your cbil score acts like a financial reputation.

Just like marks matter in academics, your credit score matters in banking.

Here are the major reasons why cbil is important.

1. Loan Approval

Banks use your credit score to decide whether they should give you a loan.

If your score is low, banks may reject your application.

2. Lower Interest Rates

People with higher scores often get loans at lower interest rates.

For example:

- Person A has a score of 800

- Person B has a score of 620

The bank is more likely to offer cheaper interest rates to Person A.

3. Credit Card Eligibility

Premium credit cards often require a strong cbil score.

A good score improves your chances of approval.

4. Faster Processing

People with excellent credit profiles may get instant approvals for loans and cards.

5. Better Negotiation Power

A strong financial profile allows you to negotiate:

- Interest rates

- Credit limits

- Processing fees

- Loan terms

Factors That Affect Your CBIL Score

Many people think only missed EMIs affect their score.

In reality, several factors influence your cbil score.

1. Payment History

This is the most important factor.

If you pay your EMIs and credit card bills on time, your score improves.

Late payments negatively impact your profile.

2. Credit Utilization Ratio

This means how much of your credit limit you are using.

Example:

- Credit card limit = ₹1,00,000

- Usage = ₹90,000

This means your utilization ratio is 90%, which is considered risky.

Experts recommend keeping usage below 30%.

3. Number of Loans

Having too many loans at the same time may reduce your score.

4. Loan Inquiries

Every time you apply for a loan, lenders check your credit report.

Too many applications within a short period may signal financial stress.

5. Length of Credit History

Older credit accounts generally help improve your score because they show long-term financial discipline.

6. Loan Mix

A balanced combination of secured and unsecured loans can positively impact your profile.

Examples:

Secured Loans

- Home loan

- Car loan

- Gold loan

Unsecured Loans

- Personal loan

- Credit card

How to Check Your CBIL Score?

Checking your cbil score is now very easy.

You can check it online through official credit bureau websites and financial apps.

Steps to Check Your Score

Step 1: Visit the Official Website

Go to the official CIBIL website.

Step 2: Register Yourself

Provide:

- Name

- Mobile number

- PAN card details

- Email address

- Date of birth

Step 3: Verify Identity

You may need OTP verification.

Step 4: Access Your Credit Report

Once verified, you can view your score and detailed credit report.

Many fintech apps also offer free cbil score checking services.

What Is Included in a CBIL Report?

Your credit report contains detailed financial information.

Personal Information

- Name

- PAN number

- Address

- Mobile number

- Employment details

Loan Information

- Active loans

- Closed loans

- EMI history

- Outstanding balances

Credit Card Details

- Credit limit

- Usage amount

- Payment history

Enquiry Information

This section shows how many times lenders checked your report.

How to Improve Your CBIL Score?

If your score is low, don’t worry.

Improving your cbil score is possible with financial discipline.

1. Pay EMIs on Time

Always pay:

- Loan EMIs

- Credit card bills

- Buy Now Pay Later dues

Timely repayment is the biggest factor in improving your score.

2. Reduce Credit Card Usage

Avoid maxing out your credit cards.

Try to keep utilization below 30%.

3. Avoid Multiple Loan Applications

Applying for many loans together can negatively affect your profile.

4. Maintain Old Credit Accounts

Do not close old credit cards unnecessarily.

Older accounts help build strong credit history.

5. Monitor Your Credit Report

Check your report regularly for:

- Errors

- Wrong loan entries

- Fraudulent activities

If you find mistakes, raise a dispute immediately.

6. Maintain a Healthy Loan Mix

Too many unsecured loans may appear risky.

Balance your borrowing profile wisely.

Common Mistakes That Damage Your CBIL Score

Many people unknowingly make financial mistakes that hurt their credit profile.

Missing EMI Payments

Even one missed EMI can damage your score.

Paying Only Minimum Due

Paying only the minimum amount on credit cards increases debt burden.

Using Full Credit Limit

High credit utilization signals financial stress.

Frequently Switching Credit Cards

Too many new accounts can reduce score stability.

Ignoring Errors in Credit Report

Incorrect information can unfairly reduce your score.

Difference Between CBIL and CIBIL

Many people search for “cbil,” but the correct spelling is “CIBIL.”

Here is the difference:

| Term | Meaning |

| CBIL | Common spelling/search variation |

| CIBIL | Official credit bureau in India |

So, if you search for cbil score, you are most likely referring to the official CIBIL score.

What Is a Good CBIL Score for Different Loans?

Different lenders may have different eligibility requirements.

However, here are general expectations.

Personal Loan

Recommended score:

750+

Home Loan

Recommended score:

750 to 800+

Car Loan

Recommended score:

700+

Credit Card

Recommended score:

700+

Higher scores improve approval chances significantly.

Can You Get a Loan With a Low CBIL Score?

Yes, but it may be difficult.

Some lenders still offer loans to people with lower scores, but:

- Interest rates may be higher

- Loan amount may be lower

- Processing may take longer

- Extra documentation may be required

Improving your score before applying is always a better strategy.

How Long Does It Take to Improve a CBIL Score?

Improving a cbil score takes time and consistency.

Small improvements may appear within a few months.

Major recovery after defaults may take 12 to 24 months.

Consistency is the key.

If you regularly:

- Pay bills on time

- Reduce debt

- Avoid unnecessary loans

your score gradually improves.

CBIL Score and Credit Cards

Credit cards can either improve or damage your score.

How Credit Cards Help

- Build credit history

- Improve repayment track record

- Increase credit profile strength

How They Hurt

- Late payments

- Overspending

- High utilization

- Minimum due habit

Using credit cards responsibly is extremely important.

CBIL Score for Students and Young Adults

Many young people think credit scores matter only later in life.

That is incorrect.

Starting early helps build a stronger financial future.

Students and young professionals can improve their profile by:

- Using beginner credit cards responsibly

- Paying bills on time

- Avoiding unnecessary debt

- Maintaining financial discipline

A strong cbil score at a young age can help later with:

- Home loans

- Business loans

- Car loans

- Premium credit cards

Is Checking Your CBIL Score Safe?

Yes.

Checking your own score is called a soft inquiry and does not damage your credit profile.

However, when lenders check your report for loan approval, it becomes a hard inquiry.

Too many hard inquiries can slightly reduce your score.

Digital Lending and the Importance of CBIL

India’s fintech industry is growing rapidly.

Today, instant loans and Buy Now Pay Later services are easily available.

But every financial activity contributes to your credit history.

That means irresponsible borrowing can damage your profile quickly.

As digital finance expands, maintaining a healthy cbil score is becoming even more important.

Myths About CBIL Score

There are many misconceptions about cbil.

Let’s clear some common myths.

Myth 1: Checking Your Own Score Reduces It

False.

Self-checking does not hurt your score.

Myth 2: Debit Cards Improve Credit Score

False.

Debit card usage is not included in credit reports.

Myth 3: Income Directly Decides Your Score

False.

Your repayment behavior matters more than income.

Myth 4: Closing Credit Cards Always Helps

False.

Closing old cards may reduce credit history length.

Future of Credit Scoring in India

The financial system in India is evolving rapidly.

In the future, credit evaluation may include:

- Digital payment behavior

- Utility bill payments

- Online transaction history

- Alternative financial data

As financial technology grows, credit scoring systems may become more advanced and personalized.

Final Thoughts

Understanding cbil is extremely important in today’s financial world.

Your credit score is more than just a number.

It represents your financial discipline, repayment habits, and overall trustworthiness in the banking system.

Whether you want:

- A home loan

- A car loan

- A personal loan

- A business loan

- A premium credit card

your cbil score plays a major role.

Maintaining a healthy score requires:

- Timely repayments

- Controlled spending

- Responsible borrowing

- Regular credit monitoring

If you start managing your finances wisely today, you can build a strong credit profile that benefits you for years.

So the next time you search for cbil, remember that understanding and improving your credit score can open the door to better financial opportunities and long-term financial stability